I’ll never forget the day a colleague called me in frustration after a parking lot incident several years ago. Another driver had backed into her car, causing several thousand dollars in damage. She had liability coverage but had dropped both comprehensive and collision to save money. The result? She was responsible for the entire repair bill. That conversation became a turning point in how I explain these two important types of auto insurance coverage to others.

In 2026, with vehicle repair costs continuing to rise due to advanced safety technology, cameras, sensors, and complex materials, understanding the difference between comprehensive and collision coverage is more important than ever. Many drivers remain unsure when they need each type — or whether they need them at all.

This comprehensive guide will clarify the differences, help you determine what makes sense for your specific situation, and provide practical frameworks for making informed decisions that balance protection with affordability.

Understanding the Basics of Physical Damage Coverage

Auto insurance can be confusing, but comprehensive and collision coverage serve two distinct purposes. Both are considered “physical damage” coverages, meaning they pay for repairs to your own vehicle rather than damage you cause to others (which is covered by liability insurance).

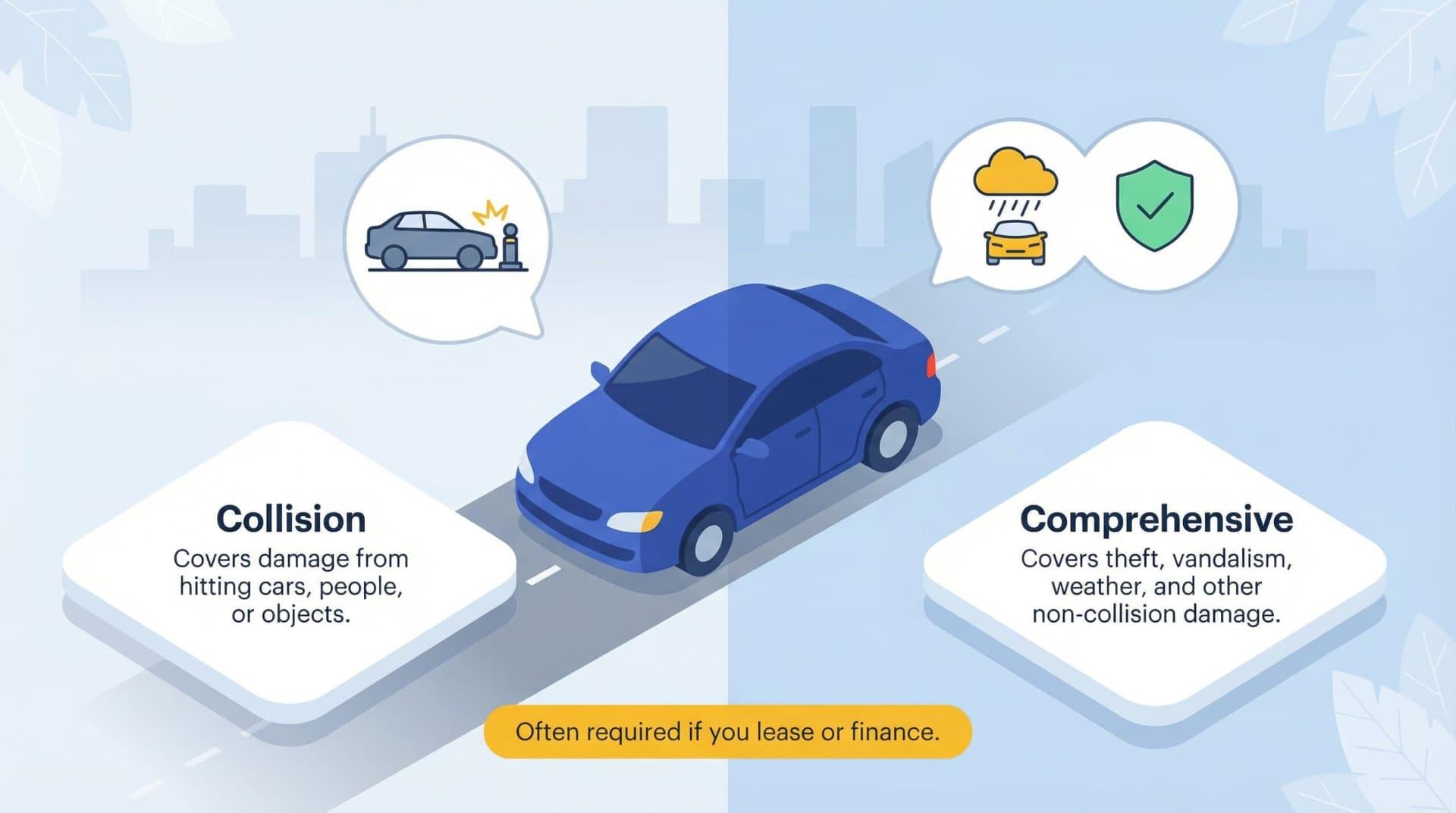

Collision Coverage pays for damage to your vehicle resulting from a collision with another vehicle or object, regardless of who is at fault.

Comprehensive Coverage (sometimes called “other than collision” or OTC) covers damage from events not involving a collision, such as theft, vandalism, fire, hail, falling objects, or animal strikes.

While they work together to protect your vehicle, they address completely different types of risks.

Detailed Comparison: Side-by-Side Analysis

1. What Each Coverage Includes

Collision Coverage:

- Crashes with other vehicles

- Single-vehicle accidents (hitting a pole, guardrail, tree, or curb)

- Rollover accidents

- Damage from potholes (in many cases)

- Damage sustained while your car is being towed or transported

Comprehensive Coverage:

- Vehicle theft or attempted theft

- Vandalism and malicious damage

- Fire or explosion

- Weather-related damage (hail, windstorms, flooding)

- Falling objects (trees, branches, rocks)

- Animal collisions (deer, birds, etc.)

- Glass breakage from non-collision causes

- Civil commotion or riot damage

2. When Coverage Applies

Collision coverage activates when your vehicle is in motion and involved in an impact. Comprehensive coverage applies to incidents where your vehicle is typically stationary or affected by external forces beyond a typical traffic collision.

3. Claims Process and Deductibles

Both coverages are usually subject to a deductible. You can often choose different deductible amounts for each. Comprehensive claims are frequently less expensive and may have lower deductibles in practice.

4. Impact on Premiums

Collision coverage is generally more expensive than comprehensive because collision claims tend to be more frequent and costly. However, the actual cost depends heavily on your vehicle’s value, make, model, and your driving record.

Key Factors to Consider When Deciding Coverage

Vehicle Value and Age This is often the most important factor. As vehicles depreciate, the cost-benefit analysis changes significantly.

- New vehicles (0–3 years old): Both coverages are usually recommended

- Mid-life vehicles (4–8 years old): Evaluate based on current market value

- Older vehicles (9+ years old): Often makes financial sense to drop one or both

Your Financial Situation Ask yourself honestly: If my car were totaled tomorrow, could I afford to replace it without insurance? Your answer should heavily influence your decision.

Geographic and Environmental Risks

- High hail areas (parts of Texas, Colorado, Midwest) → Comprehensive is essential

- High theft areas → Comprehensive becomes more valuable

- Urban vs. rural driving patterns affect collision risk significantly

Lifestyle and Usage Patterns Daily long-distance commuters face higher collision risk. People who park on the street rather than in garages may need stronger comprehensive protection.

Real-World Scenarios and Recommendations

Scenario 1: New or Relatively New Vehicle For a car less than 5–6 years old with significant remaining value, carrying both collision and comprehensive is usually the prudent choice. The cost of these coverages is typically reasonable compared to the potential repair or replacement expenses.

Scenario 2: Paid-Off Mid-Range Vehicle If your car is worth $8,000–$15,000 and paid off, carefully run the numbers. Many people choose to keep comprehensive while dropping collision, especially if they have an emergency fund.

Scenario 3: High-Mileage Older Vehicle For cars worth less than $4,000–$6,000, most financial experts recommend dropping both coverages and redirecting the premium savings into a dedicated vehicle repair or replacement fund.

Cost-Benefit Analysis in 2026

Modern vehicle repair costs have increased substantially. A relatively minor collision can easily result in $5,000–$12,000 in repairs due to cameras, sensors, and aluminum construction. This reality makes both coverages more relevant for many drivers than they were a decade ago.

Typical annual premium ranges (highly variable):

- Collision: $400–$1,400+

- Comprehensive: $150–$750+

Decision-Making Framework

Questions to Guide Your Choice:

- What is my vehicle’s current market value?

- Could I comfortably replace it out-of-pocket if needed?

- What specific risks am I most exposed to?

- How much would these coverages actually cost me?

- What is my overall financial comfort level with risk?

Recommended Approach:

- Keep both for newer, valuable vehicles

- Consider dropping collision first as vehicles depreciate

- Maintain comprehensive longer in high-risk environments

- Re-evaluate your decision annually as your vehicle ages

Common Mistakes to Avoid

- Dropping coverage based solely on age without considering actual value

- Choosing unrealistically high deductibles you couldn’t pay comfortably

- Assuming liability coverage alone is sufficient for full protection

- Not understanding how these coverages interact with your overall policy

- Failing to review coverage when life circumstances or vehicles change

Smart Management Strategies

- Choose appropriate deductibles based on your savings

- Take advantage of multi-policy (bundling) discounts

- Maintain good credit and a clean driving record

- Install anti-theft devices where appropriate

- Consider usage-based insurance programs

- Review your policy annually with your agent or broker

Final Thoughts

Comprehensive and collision coverage serve different but equally important purposes in protecting your vehicle investment and your financial well-being. Understanding the distinction allows you to make informed, personalized decisions rather than defaulting to whatever your insurer recommends or what you’ve always done.

Rather than automatically keeping or dropping these coverages, take time to evaluate your specific situation, vehicle value, risk factors, and financial comfort level. The right combination can provide valuable peace of mind without unnecessarily straining your budget.

If you’re reviewing your auto insurance in 2026, I strongly encourage you to gather detailed quotes that clearly break down comprehensive and collision options and discuss them thoroughly with a knowledgeable insurance professional. Feel free to share details about your vehicles, driving habits, location, or particular concerns, and I’d be happy to offer more targeted guidance based on common scenarios drivers face this year.

Making thoughtful decisions about comprehensive and collision coverage is an important part of responsible vehicle ownership. With the right approach, you can protect what matters most to you while maintaining control over your insurance costs and financial future.